All Categories

Featured

Table of Contents

Insurance provider won't pay a minor. Rather, think about leaving the cash to an estate or trust. For more in-depth details on life insurance coverage get a duplicate of the NAIC Life Insurance Policy Customers Overview.

The internal revenue service puts a limit on just how much money can go into life insurance policy premiums for the policy and exactly how swiftly such costs can be paid in order for the policy to keep all of its tax advantages. If certain limitations are gone beyond, a MEC results. MEC insurance policy holders may go through taxes on circulations on an income-first basis, that is, to the level there is gain in their policies, in addition to charges on any taxed amount if they are not age 59 1/2 or older.

Please note that superior fundings accrue passion. Income tax-free treatment additionally assumes the loan will eventually be pleased from earnings tax-free fatality benefit profits. Loans and withdrawals minimize the policy's money value and death advantage, might cause certain plan benefits or cyclists to end up being inaccessible and may raise the possibility the policy might gap.

4 This is given via a Long-term Care Servicessm biker, which is readily available for a surcharge. Furthermore, there are restrictions and limitations. A client may get the life insurance, yet not the motorcyclist. It is paid as an acceleration of the survivor benefit. A variable universal life insurance policy agreement is an agreement with the main purpose of giving a survivor benefit.

Who offers Whole Life Insurance?

These portfolios are closely handled in order to satisfy stated investment objectives. There are charges and costs connected with variable life insurance contracts, consisting of death and threat costs, a front-end tons, administrative costs, financial investment administration costs, surrender charges and charges for optional motorcyclists. Equitable Financial and its associates do not offer lawful or tax guidance.

And that's terrific, because that's exactly what the death benefit is for.

What are the advantages of entire life insurance coverage? One of the most enticing advantages of acquiring a whole life insurance plan is this: As long as you pay your premiums, your death benefit will never ever run out.

Believe you do not need life insurance policy if you do not have kids? You might want to believe once more. It might seem like an unneeded expenditure. However there are numerous advantages to living insurance, also if you're not supporting a family. Right here are 5 reasons you need to purchase life insurance policy.

What is the most popular Retirement Planning plan in 2024?

Funeral expenditures, interment expenses and clinical expenses can include up. Permanent life insurance coverage is offered in various amounts, so you can select a death advantage that satisfies your demands.

Figure out whether term or permanent life insurance is right for you. Then, obtain an estimate of how much protection you may need, and exactly how much it might cost. Locate the best amount for your budget plan and satisfaction. Locate your quantity. As your individual situations adjustment (i.e., marital relationship, birth of a kid or work promo), so will your life insurance needs.

Essentially, there are two sorts of life insurance policy intends - either term or long-term plans or some combination of both. Life insurance providers use various kinds of term plans and standard life plans in addition to "passion sensitive" items which have become extra widespread since the 1980's.

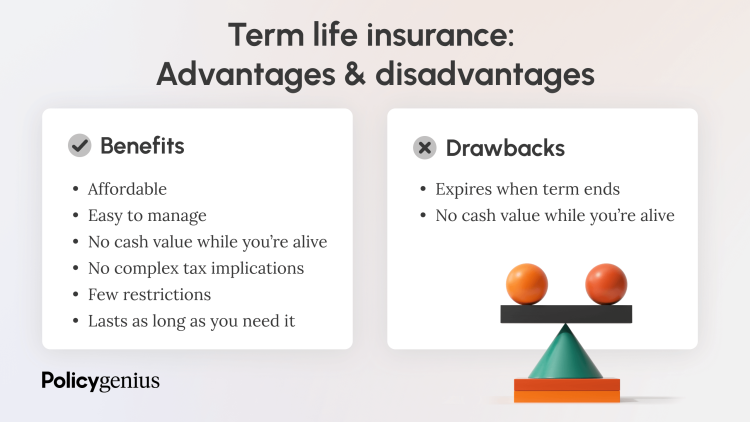

Term insurance provides protection for a specified amount of time. This period could be as brief as one year or offer coverage for a certain variety of years such as 5, 10, two decades or to a specified age such as 80 or sometimes approximately the oldest age in the life insurance policy mortality tables.

Why should I have Estate Planning?

Presently term insurance prices are very competitive and amongst the lowest traditionally experienced. It should be noted that it is an extensively held belief that term insurance coverage is the least expensive pure life insurance policy protection offered. One requires to examine the policy terms carefully to make a decision which term life alternatives appropriate to meet your specific scenarios.

With each new term the costs is increased. The right to restore the policy without evidence of insurability is an essential advantage to you. Or else, the threat you take is that your wellness may wear away and you might be unable to acquire a plan at the same prices and even at all, leaving you and your beneficiaries without protection.

The length of the conversion period will differ depending on the type of term plan bought. The costs price you pay on conversion is generally based on your "present achieved age", which is your age on the conversion day.

Under a level term policy the face quantity of the plan continues to be the exact same for the entire period. Typically such plans are sold as home mortgage protection with the amount of insurance coverage decreasing as the balance of the home mortgage decreases.

Senior Protection

Typically, insurance companies have actually not can transform costs after the plan is offered. Since such policies may continue for years, insurance providers have to use conservative mortality, interest and cost rate quotes in the costs estimation. Adjustable costs insurance coverage, nevertheless, allows insurance firms to use insurance policy at lower "existing" premiums based upon less conventional presumptions with the right to transform these costs in the future.

While term insurance policy is made to offer protection for a defined time period, permanent insurance policy is developed to offer coverage for your whole life time. To maintain the premium rate level, the premium at the more youthful ages surpasses the real expense of security. This added premium develops a book (money worth) which helps pay for the policy in later years as the expense of security increases over the costs.

The insurance policy firm spends the excess costs bucks This type of policy, which is in some cases called cash worth life insurance coverage, produces a cost savings aspect. Cash money values are essential to a long-term life insurance coverage policy.

{kind=link}

Latest Posts

Life Insurance Company Expenses

Instant Term Life Insurance Quote

Free Instant Whole Life Insurance Quote